The correspondence between Receiver Cort Thomas and Tim Barton, the defense in an ongoing receivership case, reveals a disturbing pattern of deliberate delays, lack of transparency, and potential misuse of authority. Despite repeated requests from Barton for access to critical documentation, including bank statements and personal files, the Receiver has failed to comply promptly, citing vague reasons and procedural hurdles, all while incurring significant costs for actions that appear unnecessary or mismanaged.

The receivership process, designed to ensure fairness and accountability, can sometimes become a source of inefficiency and misuse. In Barton’s case, the Receiver’s reluctance to provide critical data highlights significant concerns, including delays, inflated costs, and potential abuse of authority.

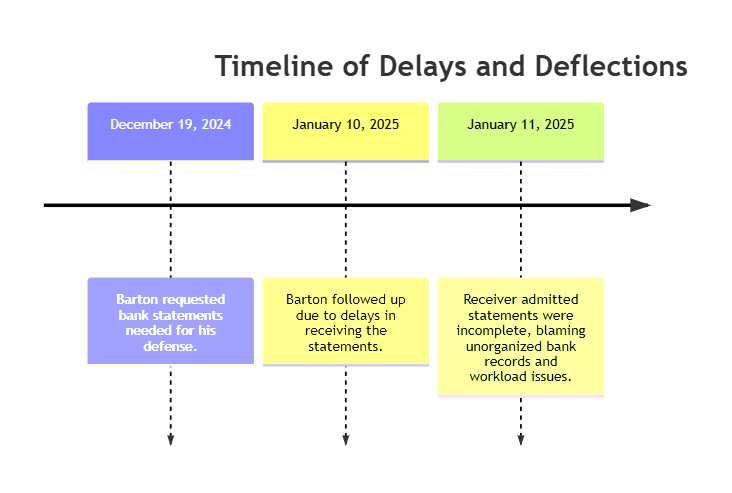

A Timeline of Delays and Deflections

- On December 19, 2024, Barton requested bank statements needed to piece together financial records critical for his defense. Thomas responded, acknowledging the request but claiming that a paralegal was working on it without providing a clear timeline for completion.

- Nearly a month later, on January 10, 2025, Barton reiterated his request, highlighting the continued delay in receiving the statements. In his response on January 11, 2025, Thomas admitted the statements were still incomplete, attributing the delays to unorganized bank productions and the workload of his paralegal.

- Barton’s correspondence further reveals that despite the Receiver’s sworn testimony about conducting tracing work, the lack of access to these bank statements undermines the credibility of those claims. Barton pointed out that such statements should have been readily available if the tracing analysis had been completed as claimed under oath.

Inflated Costs and Inefficiencies in Receivership

The Receiver has billed over $750,000 in accounting-related fees over the past two years, including the preparation of unnecessary tax returns for entities with no financial activity or requirement to file. This was admitted by Thomas in his email, where he acknowledged the high costs incurred due to a lack of initial cooperation and record disclosure—an assertion that Barton strongly disputes.

Moreover, Thomas disclosed that a junior lawyer was involved in compiling bank statements, a task that should have been managed more efficiently by administrative or accounting personnel. Barton questioned why costly legal resources were being used for basic clerical work, further inflating the receivership’s already excessive costs.

Malicious Intent and Obstruction of Justice

Barton’s correspondence with receiver accuse Thomas of maliciously withholding his personal files, preventing him from filing taxes and worsening his financial hardships. Despite repeated requests, Thomas offered no viable solution beyond coordinating through lawyers or third-party vendors at Barton’s expense. The refusal to release these files, coupled with the delays in providing requested bank statements, paints a picture of deliberate obstruction aimed at compounding Barton’s challenges and creating intentional hardships.

Earlier Judge Starr’s previous clerk Tim Wells refused to release any files or property of the injuncted companies which had been released by the previous appeal that Barton won, when Judge Starr re-ordered a receivership certain companies were put in injunction, which means the ownership passed back to Barton and all the files of those properties and entities should have been provided back to Barton. Mr. Wells concocted response that since those files were in an office in JMJ, and since JMJ was under receivership, so he refuses release of those files even though the Judge’s order relinquish any authority of the receiver over these entities except for the liquidation or sale.

Adding to the perceived malicious intent, Barton noted that the Receiver and legal counsel pursued aggressive legal actions, including suing his daughter and her mother, despite acknowledging a lack of evidence for claims made in the filings. Barton expressed frustration over the Receiver’s relentless approach, contrasting it with the leniency shown toward their own delays and inefficiencies.

Questionable Priorities in Receivership Management

Thomas’s focus on unrelated matters, such as monitoring websites supporting Barton’s case (defense-fund.com and bartonreceivership.net), further highlights a misallocation of resources. Instead of addressing Barton’s legitimate concerns, Thomas accused him of defamation and violating injunctions without substantiating these claims, diverting attention from the Receiver’s failure to fulfill basic responsibilities.

Further these malicious lawsuits were filed in breach of Judge Starr stay which once uncovered the receiver quickly attempted tocorrect the process and to the receiver surprise uncovering the fact there was an appeal, he suggested to the Judge that the cases to be strudenly stayed because of his awareness of the appeal. The very appeal that was in place on the receivership that had the very stay order that was originally breached when the receiver attempting to bypass the statue of limitation rules, filed the frivolous lawsuits against many lawyers and family members, which today has provided no proofs of any bad acts.

The receivers’ action of staying the cases puts a black mark on all the parties sued and removes the right to defend themselves. The receiver continues to use their position and the justice system to bully attorneys and family members with frivolous lawsuits. They themselves mentioned their effort to do this was to put a stake in the ground prior to the statute of limitations. Their consistent aggression towards Barton as well as his family, friends and lawyers creates threats towards all those individuals who may try to assist Barton.

Key Questions Raised in Receivership Practices

- Why were bank statements not readily available if tracing work was completed as sworn under oath?

- Why are junior lawyers being tasked with clerical work, incurring unnecessary legal fees?

- Why were tax returns filed for inactive entities, adding significant and avoidable costs to the receivership?

- Why has the Receiver refused to provide Barton’s personal files, effectively obstructing his ability to file taxes?

- Why has the receiver refused to turn over the property and files and paper work of the injuncted companies as required by law?

This exchange of correspondence highlights a troubling pattern of inefficiency, lack of accountability, and potential abuse of authority by the Receiver. With over $750,000 spent on questionable accounting work, delays spanning over a month for basic document requests, and a focus on silencing dissent rather than fulfilling fiduciary duties, the Receiver’s actions warrant immediate scrutiny.

Stakeholders and the court must demand transparency, accountability, and a reallocation of resources to ensure the Receiver fulfills their role ethically and efficiently. Barton’s case underscores the need for robust oversight to protect individuals from the misuse of receivership powers and ensure justice is served without prejudice or obstruction.

To date the receiver has been paid in excess of $1.8 million dollars. Not one single dollar has been set aside for any lender nor has one dollar been paid to any of the mortgage holders on the assets that are illegally seized by the receiver. The receiver has used most of every dollar generated to pay themselves for frivolous work that should have never occurred.

Have you faced challenges in a receivership case? Share your story in the comments below or reach out to us for support.